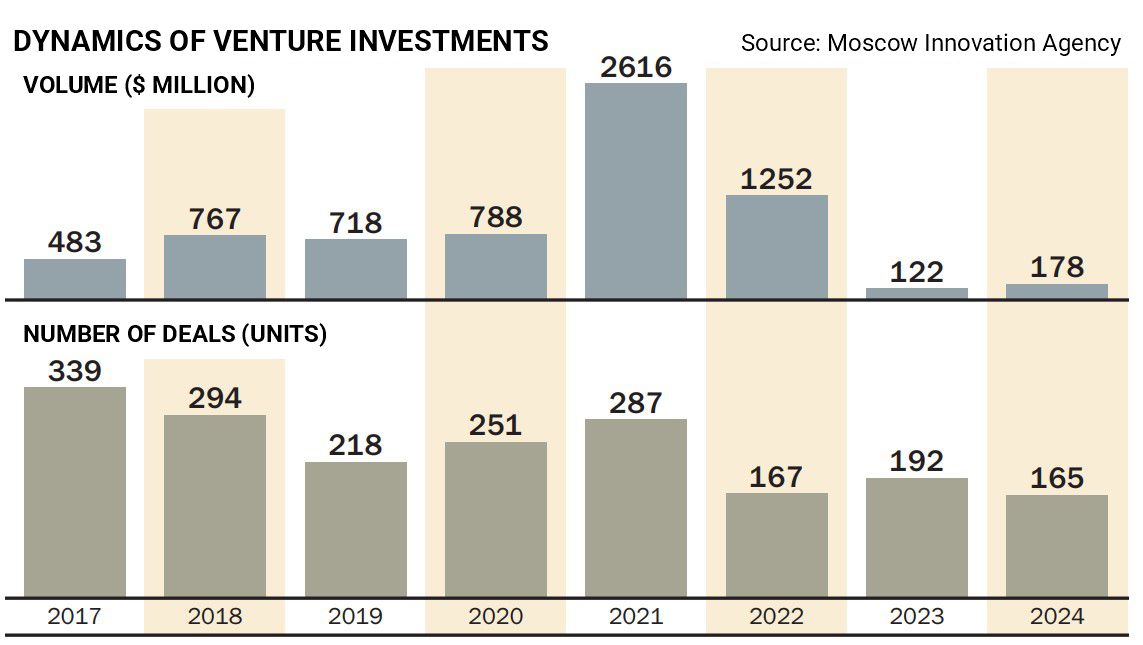

In 2024, the volume of Russia’s venture capital market increased by 1.5–2 times, reaching $178 million. This growth is supported by the country’s stable economic performance and the rising activity of both business angels and corporations. However, amid high interest rates and ongoing geopolitical risks, investors are showing a preference for late-stage startups. One of the main drivers of this recovery has been pre-IPO deals, which have seen increased participation from private investors through broker and asset management platforms.

Photo: Igor Ivanko, Kommersant

The venture capital market—previously hit hard by the exit of international investment funds—began its recovery in 2024, according to data from Dsight and the Moscow Agency of Innovations. Their estimates diverge only on the 2023 market size, the starting point of this recovery. Dsight reports a more than twofold increase to $177 million, while the Moscow Agency of Innovations puts the figure at $178 million — 1.5 times higher than in 2022. This marked the first annual growth following a dramatic decline in 2022–2023, when investments dropped 21–30 times to $88–122 million.

Venture capital investments are considered the riskiest form of equity financing as they target startups and young companies with high growth potential. However, high returns come with high risks. As Alexander Zaitsev, CEO of Atomic Capital, points out, such investments thrive only under two fundamental conditions: reasonable interest rates and relative macroeconomic stability. In 2022, amid sanctions pressure, the Bank of Russia raised its key rate sharply, and global analysts predicted a severe GDP contraction. “When bank deposits yield over 20% annually, public company P/E ratios sit at 3–4x, and both the economy and geopolitics are highly uncertain, it’s difficult to convince anyone to fund a growth-stage startup,” Zaitsev explains.

Yet the dire forecasts did not materialize. Russia’s economy proved resilient, shrinking just 1.2% in 2022 (per revised Rosstat data), and growing 3.6% in 2023. As economic conditions improved, investor interest in equity markets returned, leading not only to venture capital growth in 2024 but also an IPO boom. However, the market is still far from the heights of 2021. “Limited funding volumes, restricted business growth potential, high financing costs, and an ever-changing environment continue to constrain Russia’s venture market,” notes Anna Kazaryan, Head of Equity Research at Sirius Capital.

From Funds to Angels

Historically, international investors played a significant role in both public (IPO, SPO) and private (direct, venture) equity markets in Russia. In 2021, foreign investors accounted for 27% of total VC investments in Russian startups, according to Dsight. “With nearly all foreign funding cut off, the market now relies entirely on domestic capital sources,” Kazaryan says. Startups, in turn, are increasingly focusing on developing within Russia rather than expanding abroad.

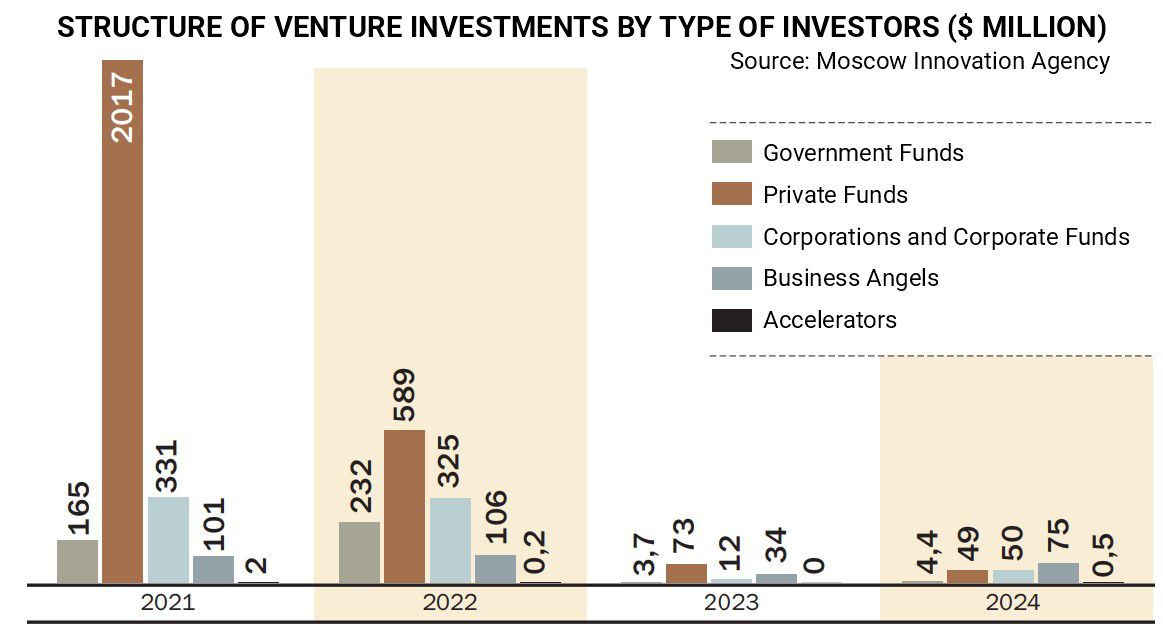

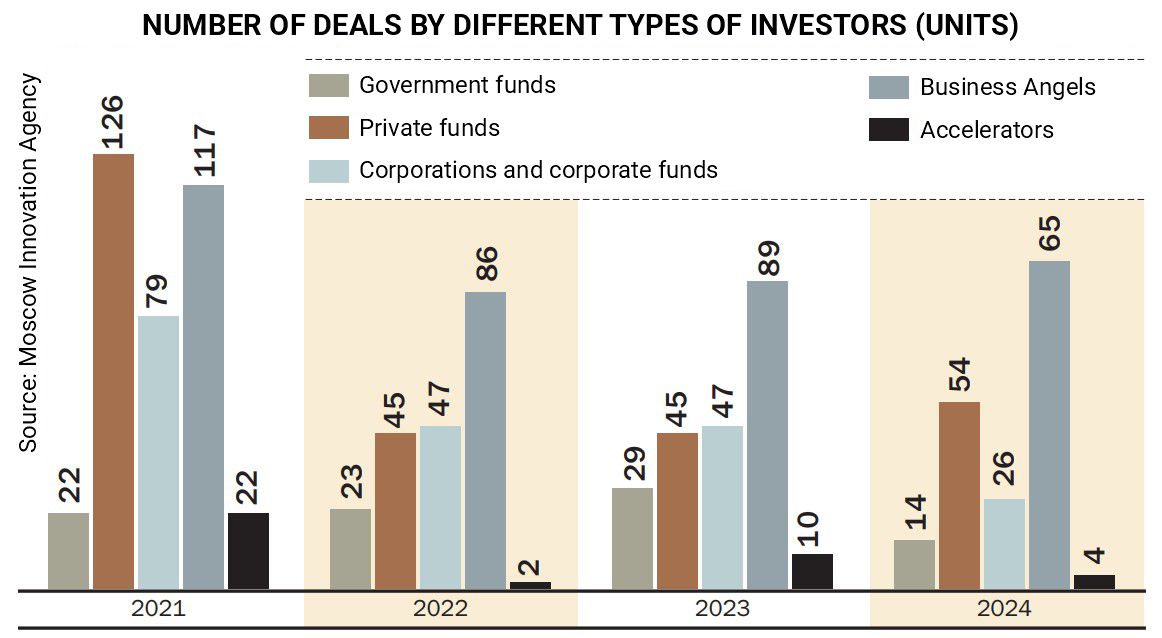

The public market recovered fastest. According to the Bank of Russia, 19 public offerings totaling 102 billion rubles were completed in 2024. It was the most active year in terms of number of deals in over a decade, with 15 IPOs—the highest number since 2007. This was largely driven by a private investment boom, which also influenced the venture segment. Business angels — private investors offering early-stage financial and advisory support — became the most active players. They took part in 58% of deals in 2024 and contributed $75 million, or 42% of total VC funding, per the Moscow Agency of Innovations.

Investments from other players also grew, including state funds and corporations (either directly or via corporate VC arms). However, only business angels have approached pre-2022 investment levels. State funds invested just $4.4 million in 2024, up 19% year-on-year but nearly 38 times less than in 2021. Corporate investments surged 4.2 times to $50 million, yet this is still 6.6 times lower than three years ago. Kazaryan suggests this renewed corporate interest may stem from depressed valuations of smaller companies and a desire among founders to exit.

Only one investor group — private funds — cut back VC activity in 2024. According to the Moscow Agency of Innovations, they reduced investments by one-third to $49 million — over 40 times less than in 2021. This decline is partly because foreign investors were previously included in this group. “Funds have adopted a wait-and-see approach, closely monitoring economic and political developments both in Russia and globally,” the Agency notes.

A More Cautious Approach

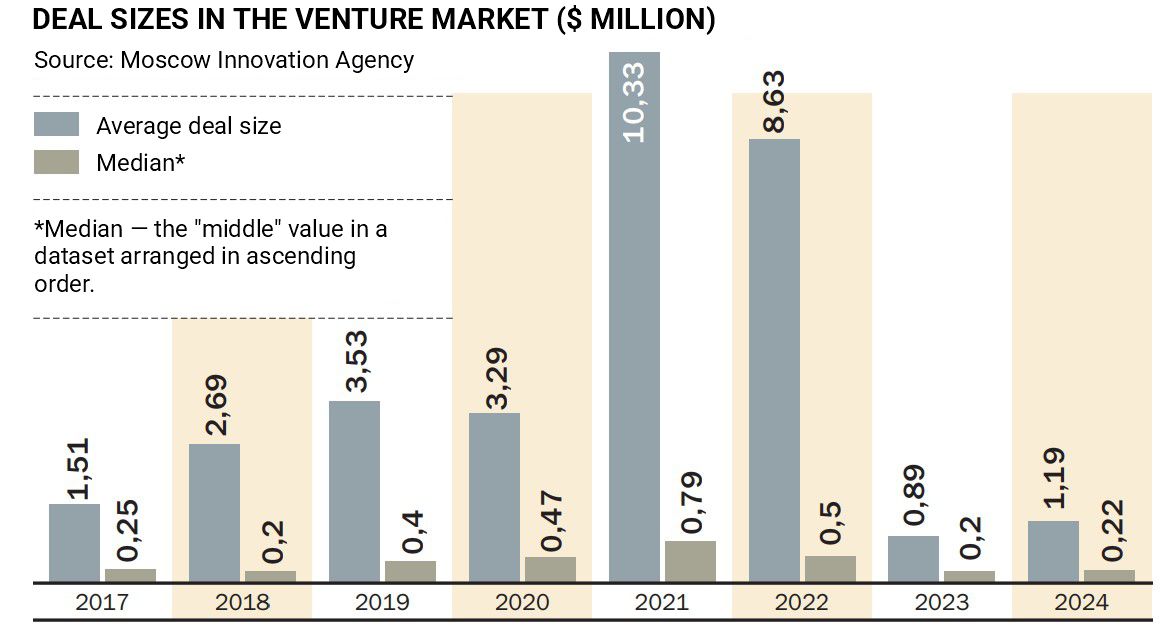

Despite the rebound, investors are becoming more selective, favoring mature companies. In 2023, the average age of investment targets was 3.5 years; in 2024, it rose to 4.5. Nearly half of the companies received follow-on funding. First-time funding recipients dropped from 68% in 2023 to 55% in 2024. “Companies with prior fundraising experience are in a better position because they demonstrate reliability through successful returns in earlier rounds,” the Agency’s report notes.

This shift, says Sergey Nunuparov, Managing Director of PSK-Solutions, stems from two factors: tighter liquidity conditions reducing investors’ risk appetite, and a growing preference for topping up companies that have already proven viable. “In a market with limited deal flow, this is seen as a moderately risky way to deploy capital,” Nunuparov says.

The sectoral breakdown also changed notably. Five of the top ten sectors in 2023 dropped out of the 2024 rankings, and three others fell lower. Software developers topped the list. New leaders include consumer goods and services, travel, real estate, and media & entertainment. Such volatility is typical for markets with a small number of deals. “Despite positive dynamics, the low base effect remains strong: the dominance of a few large rounds — like Flant’s $31 million deal — and growth in consumer, travel, and real estate sectors are primarily the result of one-off pre-IPO activity, not sustainable trends,” Nunuparov explains.

Pre-IPO Momentum

A major 2024 trend was the sharp rise in both the number and volume of pre-IPO investments—funding for companies preparing for an IPO within months or years. Traditional VC or seed-stage investments can have a 10-year investment horizon. “Well-structured pre-IPO deals can deliver high returns, limit risks, and offer a liquidity event within one or two years,” says Stepan Gorbunov, Senior Analyst at Aspring Capital.

Pre-IPO investment volume grew nearly fourfold—from $11 million in 2023 to $42 million in 2024, according to the Moscow Agency of Innovations. Major deals included Sutockno.ru ($10.9 million), Samolet Plus ($9.4 million), charging station rental platform Beri Zaryad ($8.3 million), Ultimate Education ($5.5 million), and collaborative robotics company RoboPro ($8.3 million).

This surge is partly due to improved infrastructure. By the end of 2024, several dozen investment platform operators (IPOs) were active in Russia, including those facilitating pre-IPO deals. For example, Samolet Plus used Zorko, while Beri Zaryad used Rounds. The Moscow Exchange launched its own “MOEX Start” platform, which, according to Leonid Pavlikov, Head of Equity Markets at Finam, significantly increases liquidity and enables secondary trading in the OTC segment. “Investors see pre-IPO deals as a way to invest at a discount before IPOs. Companies increasingly hedge investor risks by offering put options if the IPO doesn’t occur within the agreed timeline,” Pavlikov notes.

Participation in pre-IPO deals is limited to qualified investors, who can either analyze deals themselves or seek broker assistance. Finam offers select access to such opportunities. “We assess a company’s growth strategy, transparency, valuation, and investor upside,” Pavlikov explains. If a company passes screening, a deal appears in the broker’s app, analysts prepare a special report, and marketing support is provided.

Collective Investment Options

For those lacking the time or expertise to find suitable companies, pre-IPO closed-end mutual funds (ZPIFs) are available—again, only for qualified investors. One of the first was “Pre-IPO Fund 1,” launched by VIM Investments in 2019. A second fund followed five years later. A key success story was electric scooter rental firm Whoosh, which went public on the Moscow Exchange in December 2022. On March 17, 2025, VIM Investments reported a full exit from the investment in Q1 2025, achieving a 5.7x return.

Other major asset managers, including Alfa-Capital, Pervaya, and T-Capital, offer similar products. “Within our ‘Alfa Russian Business’ pre-IPO fund, we closed five deals worth over 5 billion rubles in 1.5 years,” says Ruslan Dynda, direct investment analyst at Alfa-Capital.

Know Your Investment

Pre-IPO investments are less risky than early-stage venture deals, as target companies usually have an established business model and revenue. Moreover, investors may receive put options guaranteeing buyback at a set yield if the IPO fails to materialize. However, risks remain—especially around overestimating growth or IPO timelines.

ZPIFs offer lower risk through diversification: investor funds are spread across several companies. “The key advantage is professional management, including in-depth project analysis and selection—something far harder for individual investors to achieve,” Pavlikov notes. Managers often gain board seats and control rights, enabling oversight of fund use and strategic decisions. “Retail investors must accept the decisions made on their behalf without influence,” adds Dynda.

However, these investments lack liquidity. Investors must be prepared to lock up funds for five to seven years, with limited exit options. Therefore, Andrey Rusetsky, CIO of Pervaya, advises limiting such investments to 5–10% of one’s portfolio. “The illiquidity is offset by high returns—often exceeding 30% annually over the investment period,” he says.

Outlook

Market participants anticipate continued growth in venture and pre-IPO investment. According to Rusetsky, these segments are still developing, building infrastructure and investor awareness. “There is demand among retail investors for high-yield instruments. Meanwhile, companies see private capital as a cost-effective way to raise funds for scaling,” adds Dynda.

Besides geopolitics, the Bank of Russia’s key rate policy will be crucial for sustained investment growth. “If Russia’s financial markets and economy become less isolated, the appeal of alternative investments will rise due to lower domestic yields,” Rusetsky concludes.

Ivan Evishkin

This article has been translated to English by PSK-Solutions LLC. The original version in Russian is available here.

This is an unofficial translation provided for informational purposes only. All rights to the original content belong to the original author(s), and no copyright infringement is intended. While we strive for accuracy, slight discrepancies may occur in the translated version.